In Canada, an average WTI oil price of US$63-65 per barrel is required to yield a 9% after-tax return on ‘full-cycle’ costs for the oil plays shown on page 1 compared with close to US$72 in the United States (based on costs in the Fall of 2013).Interestingly, the article points to the plateauing production in the Permian Basin is plateauing. And a weak December in the Bakken according to NDRC data as outlined here by Ron Patterson at peakoilbarrel. Of course a singe data point is simply a single data point. But it does raise some interesting pricing and production possibilities for the future.

Let's take the status quo as the best predictor of future production and pricing. The Scotiabank report alludes to this by contrasting the "long-life, low decline rate assets" in Canada to the American plays which offer, "scale, but with rapid decline rates".

Now, assuming pricing remains constant, the economics of these play are as outlined. If this report is to be believed the Canadian plays are at the very least as profitable, if not more profitable then the American tight plays.

If future prices are significantly lower then we have now, then the economics of a high IP, high decline, play where growth is quickly ramped up and scaled down becomes a better bet in terms of net present value (NPV). If, however, prices are higher, then the long lived, lower IP but lower decline assets gain in value as the discount rate in any NPV calculation is offset by the appreciating value of the long lived production.

My argument is simply that the upside pricing scenario is significantly more likely to occur then the downside pricing scenario.

What will impact the price that Canadian's get on their oil?

In terms of production upside and downside misses. While the incredible run up of American production numbers from these tight oil plays has had global implications, the variability of this production is often understated.

With the documented high rates of decline, production growth is predicated on drilling growth. Project economics are often over the 2 or 3 year timescale and are thus likely to be highly price sensitive.

Ron Patterson has another great post on peakoilbarrel.com looking at how reliant the world is on the American light tight oil to maintain $100 oil:

Simply assuming that global demand does not fall; the impact of any deceleration (or decline) in American light tight oil will have material supply side implications that will exert upward price pressure. A great thing for Canadian long lived assets.

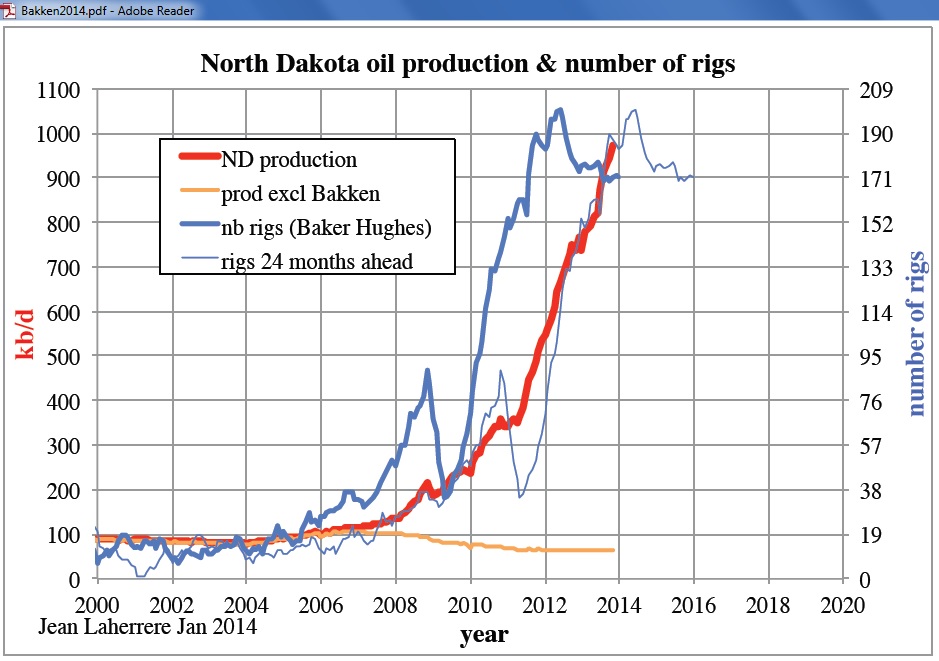

While the decline rate of tight oil wells is fairly well understood. The production rates of the entire play is still unknown. Are their "sweet spots" that will result in future individual production rates to decline? If so, higher rates of drilling will be required to offset that. Jean Laherrere gives us this graph (below) and speculates that a 24 month shift in the number of rigs maps fairly well onto production levels; we'll soon find out if he's onto something.

Will the US maintain their incredible oil production growth? Count me as a skeptic. But this seems like a requirement if the supply side is to exert downward price pressure.

Barring a technological breakthrough that renders renewables economical (which I believe will come at some unknown point and in some unknown form) if Canadian assets offer favorable, or even comparable, economics given the status quo. Then we're looking good.

I'm still assuming the liklihood that pipelines are in place before we reach our take-away capacity is >.5. The liklihood that US light tight oil production falls and exerts upward price pressure? I'm thinking that's gotta be 50/50 over a 5-10 time frame.

Either way, I'll guess a p>.99 that those oilsands will be developed fully.

No comments:

Post a Comment