It seems to me that the Saudi's need to convince the market that their strategy is the new status quo. Period. We will produce oil if it's economical, our oil is economical down to $x, so good luck with your oil! Similar to forward guidance in monetary policy, the swing producer can only move markets with words if their actions (or more specifically, their communicated future actions) are deemed credible.

Arguments against the credibility of this new non-price supportive strategy seem to hinge on the 'break-even' fiscal story (which gets mentioned all the time and I largely ignore when it comes to KSA). However, in terms of sheer economics, market share, market power, geo-political and regional balances of power, alternative fuel viability, the KSA seems likely to pursue their market grab. At the very least we need to consider it credible until proven otherwise.

Implications of Lower Prices

Although we hear it discussed more and more, I still believe the heterogenous nature of oil market is underreported. First, defining oil is inherently difficult, what we call 'oil' is crude oil, the EIA summarizes the variety here where oil is classified according two qualitative variables: density (API) and sulfur content (sour/sweet). Sweet oil is good (less refining required to get useable product). Mid density is good (the heavier the oil the more 'energy' is contained in the carbon chain, it's a balance between energy content and difficulty in cracking it in the refining process).

The second differentiator is the price differential. In Canada we know all about this. These differentials are driven by the local quality of the oil, but also the ability of that oil to get to markets that want them. The EIA article above outlines that globally. In this article from Bloomberg describes inter-regional price differentials. Which is where things start to get a bit more interesting. First let me set this up a bit.

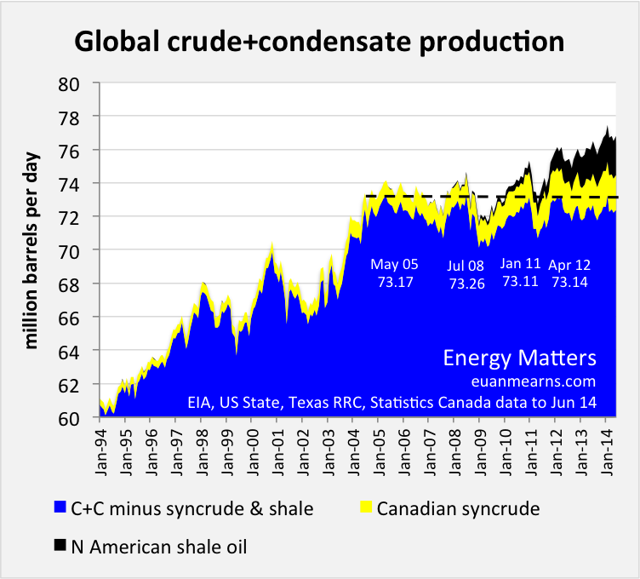

This article by Euan Mearns on Seeking Alpha points sketches out where the 'new oil' is coming from. Namely, Canada and the United States:

|

| Figure 2 Global production of conventional crude oil and condensate has not changed since May 2005 despite a prolonged spell of record high oil price. All of the growth has come from expensive LTO and tar sands. The toxic mix of high debt and losses in the LTO industry that are in the making may short circuit the global banking system again. |

So that's the set up. Why these sources of oil have been prolific is something we'll skip over (how much is ingenuity, how much is the recent steady state of $100+ oil?). But where this gets interesting is when you consider the variation in production costs.

Prices and Production Costs

Again, this is an incredibly difficult figure to make sense of. These costs vary with the factors mentioned above. The regulatory and transportation frameworks are also key. But aggregated I think we can fairly make some interesting and relevant inferences.

Decline Rates: By definition, if decline rates increase, the number of new wells that need to be brought online to maintain production levels also increases. This isn't controversial. How quickly wells decline is another difficult thing to be accurate on, however, it isn't controversial to suggest that LTO wells have significantly higher decline rates.

It will be interesting to watch how oil sands and LTO production behave if oil prices continue to hover in this lower range for a significant portion of time. You'll see capex budgets slashed in Alberta, without any real production decline (rather a reduction in growth), but how will LTO production behave?

It will depend on the fiscal health of these companies and the duration of $70ish oil, but since LTO requires drilling activity to maintain production levels, and increased drilling activity to produce the production growth we've seen, any hiccup in capex will have a much larger impact then we'd see in any other oil play.

Costs vs. Prices: Let me butcher Econ 101 here: shut down isn't justified simply when operations are cashflow negative. Rather, you have to make a few considerations. The future behaviour of both costs and price. Costs have both a sunken and operating portion, where the sunken portion are more long run (infrastructure, regulatory, exploratory, etc.) and operating costs refer more to the actual production and transportation of oil to markets.

Again, with high decline rates comes more drilling, comes more regulatory issues, comes more infrastructure (increased production points). And these decisions happen in real time. Oil sands projects have massive upfront costs. They also have high operating costs (relatively speaking). The difference is in how the economics impact production volume.

LTO companies can immediately cut the sunken costs by reducing drilling activity. How long it takes to work through the backlog of well sites ready to go (with significant sunken costs) remains to be seen. But I have to believe that if low prices stretch through this drilling season into next year's drilling season, we're bound to find out.

Oilsands production might stagnate, but remember that massive upfront investment also results in fewer individual decisions.

Duration: Steep decline rates also mean that when a new LTO well is brought into production is more important to the lifecycle economics of the project. Rune Likvern has done alot of interesting work on decline rates and the subsequent economics. While, his overall production predictions have not come to fruition, the underlying logic still remains solid (in my eyes). In this follow up posted on Peak Oil Barrel, Rune makes some interesting points.

Most relevant here is the notion that the leverage that has enabled this massive drillout of the LTO plays in the United States are likely also conditional on the high price of oil. Now we have pressure from both the strict cost and benefit economics of the oil well, but also, the exogenously determined credit conditions. Being in the finance game I know that when some guy in some office some where gets freaked out about a negative trend, the tap can turn on and off pretty quick. Might the tap turn off quick here? It likely depends on the expected duration of these low oil prices.

Remember, LTO producers are firms, they have no access to printing presses. They dividend out their earnings. They are accountable to quarterly reports. They are not national oil producers. This makes for the most efficient model when it comes to exploiting economic plays. But when they become uneconomic? Well... we might just find out.

Conclusion

I believe we will see supply reduction and prices rebound. Over what time frame? No idea. But if the KSA won't take on the entire burden. The first domino to fall will be the US Shale producers. They've had the greatest impact on global oil production. But the nature of the oil production and the debt factor will necessitate blinking first.

No comments:

Post a Comment